The Difference Between 401(k) and 403(b) Plans

It’s always a good idea to start saving for retirement as early as possible. Two common retirement options – 401(k) and 403(b) plans – are both employer-sponsored retirement savings plans that offer tax advantages. You usually get access to only one of these options through your employer.

It’s important to know which one applies to your situation and to be aware of common retirement mistakes. If you have access to both, there are some similarities and differences to know before enrolling. You’ll also need to know the difference between a traditional and Roth account.

What Is a 401(k) Plan and How Do 401(k) Plans Work?

Congress designed 401(k) plans to encourage Americans to save for retirement. A 401(k) plan is typically offered to people by private-sector, for-profit employers. When you have a 401(k) plan, you can set regular, automated contributions from each paycheck up to a specific limit. The contribution limit for 401(k) plans is $20,500 for 2022.

Many employers match a percentage of each contribution, which essentially means you can receive free money for retirement. Employees are responsible for choosing the investments the money goes to from the selections set by the employer. Other than for specific exceptions, you can access the funds without tax penalty only at age 59 ½ or older. There are two main types of 401(k) plans, and both offer tax advantages and other benefits.

Traditional 401(k)

If you choose to contribute to a traditional 401(k), your contributions are deducted from your gross income, meaning the money comes from your payroll before any taxes are taken out. Ultimately, your taxable income is reduced. This can be a helpful benefit during your contribution years. No taxes are due from you for the money contributed or its earnings until you choose to withdraw it.

Roth 401(k)

Not all employers who offer a 401(k) plan will offer the Roth version. When you contribute to a Roth 401(k), the funds are deducted from your after-tax income, so you do not have any tax deductions for the year you make the contributions to this account. However, this also means you don’t pay any taxes when you withdraw the money or its earnings.

What Is a 403(b) Plan and How Does It Work When You Retire?

A 403(b) plan is actually quite similar to the more well-known 401(k). This retirement account was designed for specific types of employees. You may be able to acquire a 403(b) plan if you are a professor, school administrator, teacher, doctor, nurse, librarian, employee of a tax-exempt organization, or government employee.

Just like with a 401(k), you make regular, automated deductions straight from your paycheck into the account. There is a limit to the amount you can contribute. The contribution limit for 403(b) plans is $20,500 for 2022. The money you contribute is then invested. As with a 401(k), other than for specific exceptions, you can access the funds without tax penalty only at age 59 ½ or older.

Traditional 403(b)

When you contribute to a traditional 403(b) account, the contributions are tax-deferred, so you don’t have to pay tax on your contributions until it comes time to withdraw them. This can be desirable because you will be saving money while contributing to the account.

Roth 403(b)

Contributions to a Roth 403(b) account are made with after-tax income. While there is no immediate tax advantage to choosing this option, you will not have to pay taxes on the money and earnings you withdraw, as long as the withdrawals are qualified distributions.

What Is the Difference Between a 401(k) and a 403(b) Retirement Plan?

You may be wondering about the difference between these two types of retirement accounts. Typically, you will only be able to choose from one of them. If you work in the private sector, you will usually only be able to select a 401(k). If you work for the government, public schools, state colleges, or in another tax-exempt organization, you will typically only be able to choose a 403(b). Both plan types allow your money to grow tax-free.

If you find yourself in the rare situation where you get to choose between them, you should know the 401(k) and 403(b) advantages and disadvantages. It’s important to note that they share contribution limits. If you have both a 401(k) and a 403(b) account, you can still only contribute the contribution limit in total between the two accounts.

Advantages of the 401(k)

One of the main advantages of a 401(k) is that most employers will help fund contributions in some way. There are match programs where employers will match your contributions up to a certain amount. This is a great way to save extra money. Many financial advisors recommend contributing at least the amount that gets the highest match rate from your employer. Doing so allows you to get the maximum amount of “free money” for retirement.

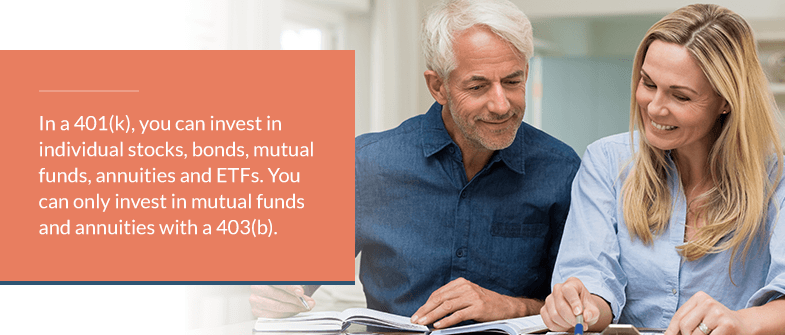

401(k) accounts typically have more investment options. In a 401(k), you can invest in individual stocks, bonds, mutual funds, annuities, and ETFs. However, with a 403(b), you can invest only in mutual funds and annuities.

Advantages of the 403(b)

Some 403(b) accounts are exempt from certain tests and other guidelines from the Employee Retirement Income Security Act (ERISA) because many employers who offer 403(b) plans do not help fund contributions. If an employer does make contributions to employee 403(b) accounts, they are subject to the same guidelines and reporting requirements as those who offer 401(k) plans.

Since non-ERISA 403(b) accounts have fewer reporting requirements, they often have lower administrative fees and expense ratios.

Contact HSC Wealth Advisors for Personalized Advice

The best thing you can do for retirement planning is to get educated on your options and begin contributing if you aren’t already. If you’re researching your options, you are already off to a good start. There is a lot more to consider, and you may be looking for additional information before deciding which option to select. When you need help with financial planning, reach out to an advisory company.

HSC Wealth Advisors is a fee-only firm, meaning we offer unbiased advice and don’t represent any one investment firm. We don’t receive commissions or compensation from any other source, so there are no conflicts of interest. You can be sure we are on your side and make decisions based on what is best for you and your money.

Our qualified team of 401(k) and 403(b) advisors near Lynchburg, Virginia, can help diversify your retirement portfolio. We are happy to help clients from Virginia and other states navigate the complicated process of saving for retirement or earning wealth after you’ve retired. Contact us today to learn more, get answers to your questions, and start on the path to retirement planning.

Joel is a CERTIFIED FINANCIAL PLANNER, Accredited Investment Fiduciary®, and a NAPFA-Registered Financial Advisor. He holds a BS from Liberty University and completed the University of Georgia – Terry College of Business' Executive Program in Financial Planning. He is passionate about offering unbiased financial advice and helping clients achieve their goals and objectives.